How QSEHRAs work

Quick summary: Employees pay for health expenses, you reimburse them tax-free.

How does QSEHRA work?

The mechanics of QSEHRA health insurance are surprisingly simple. At a high-level, employees pay for their own health expenses and you reimburse them. Here’s how it works:

- Employers design their plan and set reimbursement allowances

- Employees pay for their own health insurance and medical bills

- Employees provide proof of their expenses

- Employers reimburse the employee up to the set limit

The key to note is payments are reimbursements. Employees will pay the insurance company or doctor’s office directly and then submit a claim to get reimbursed for their expenses tax-free.

We often get questions from employers concerned about their employees having to cover high insurance premium costs on their own before receiving a reimbursement. To help, you can adjust the timing of reimbursements and setup automatic reimbursements through payroll. This way, you can get funds to your employees’ accounts before the bill is due.

The new “thing” to save the day: QSEHRA (aka the Qualified Small Employer Health Reimbursement Arrangement)

The insurance environment looked bleak for small employers in 2015 and 2016. Thankfully, however, the Small Business Administration and others continued to lobby congress to fix this problem. As a result, at the very end of President Obama’s 2nd term in December of 2016, a hodge-podge bill called the 21st Century Cures Act was passed with a provision creating the QSEHRA.

The irony is at the height of the political debate in 2017 about healthcare reform, the 21st Century Cures Act snuck through and became law without many people noticing. It was endorsed by both Republicans and Democrats and was largely seen as a fix to the unintended consequences of the ACA and a “small business friendly” provision. Similar “defined contribution” structures were included in most major Republican healthcare reform plans. We think this is important for prospective QSEHRA users to know—while healthcare reform efforts could pick up again and things could change, the highly bi-partisan nature of support for the 21st Century Cures Act means it’s probably not going away anytime soon. Plus, if large businesses can get health insurance tax-free, why can't small ones? Feels like common sense.

Now in 2025, we've see QSEHRAs take off exponentially since they began. We expect to see that same growth continue.

Optimized Benefits

Before QSEHRA, a small employer’s only option if he or she wanted to provide health benefits was to offer a traditional, one-size-fits-all group health plan. If the boss chooses Blue Cross, everyone gets Blue Cross. It’s like forcing everyone at your company to wear the same size suit:

Figure 2: For employers with less than 50 employees, getting a group plan is like forcing everyone to wear the same sized suit. Don't be like this group!

In contrast, a tax-free reimbursement plan is much more optimized. By giving cash tax-free, employees can choose their own plan. If one employee wants Blue Cross because it has his doctor in network, great! If another employee wants to move to Aetna because it handles her prescription better, no problem! Finally, if another employee already gets great coverage through his spouse, he can stay on that plan and use the reimbursements to help with medical bills.

If the plan is designed to allow for medical expense reimbursement too, employees can spend it on whatever they need (contacts, prescriptions, dental care, etc). Reimbursements go directly towards meeting employee needs, not into a pit of group plan deductibles and premiums. And if an employee doesn’t need a reimbursement, the company keeps the money. No “use or lose”. Where a traditional group plan locks people in to plans that may not fit them, a QSEHRA gives employees options and flexibility and results in greater optimization.

Combine your QSEHRA plan with a solution like Take Command's enrollment software that helps your employees discover more plans that are optimized for their needs. This ensures your dollars are being spent efficiently and that your employees are buying plans they are happy with.

What every accountant should know about QSEHRA

Table 1: Tax Savings Example

The result is that offering reimbursements through salary crush the value of the “stipend”, with over 30% of the value ($1,200/mo in this example) being wiped out in taxes. Ouch. However, with tax-free reimbursement, employees get to use the full value for their health insurance and medical expenses.

Flexible Design

QSEHRA provides immense flexibility over other benefit options. We’ll cover some of the mechanics in the requirement section but here we will focus on the benefits. For starters, in most states, group plans require employers to contribute at least 50% of the employee-only costs and require at least 75% of employees to participate. This approach can be extremely burdensome and “group savings” typically don’t kick in until an employer has over 100 employees. With a QSEHRA, there are no minimum contributions required or participation rates to maintain.

In addition, employers can typically design their QSEHRA to fit their business needs. While employers have to treat full-time employees fairly, there are a lot of levers they can pull on how much to reimburse and who gets to participate. For example, employers can vary reimbursement rates by married status. They can also chose whether to include or exclude part-time and seasonal workers. For more design options, see Reimbursement Rules below.

Budget Control

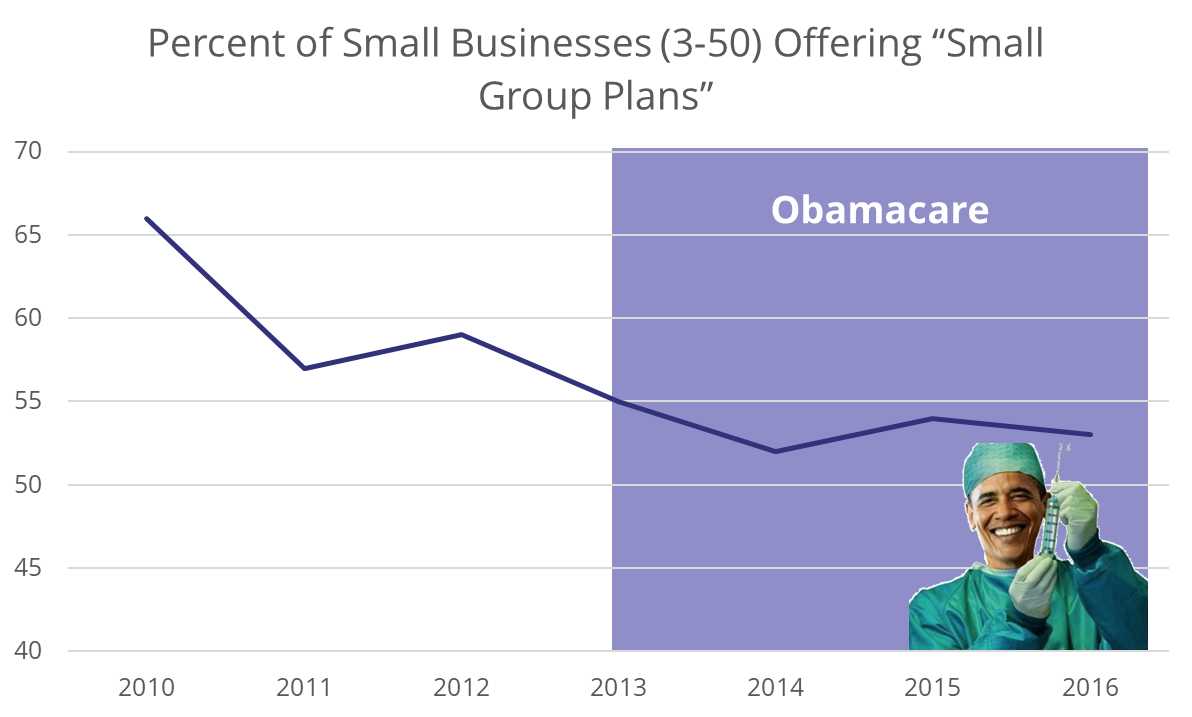

Traditional small group plan premiums have gone up an average of 30% over the last few years. When we surveyed business owners, they mentioned they felt “hopeless” and “frustrated” at this expense that was out of their control and always going up. In many states ,the minimum contribution required to maintain a group plan is up to $400/mo per employee. In fact, you can see employers have been dumping their group plans and according to KFF, the largest reason is cost:

This is where QSEHRA is truly a game-changer. Employers can set how much they want to contribute (up to the maximum amounts, discussed later) and there are never any increases unless the employer wants to increase the amount. QSEHRA is a much more budget friendly solution for small businesses and non-profits.

Pros and Cons of QSEHRA

Wondering what the pros and cons of QSEHRAs are?

QSEHRA pros and cons are critical to consider if you are assessing whether a QSEHRA is right for your small business.

| QSEHRA Pros | QSEHRA Cons |

|---|---|

Roughly 80% of our small business clients are net new to benefits, meaning that QSEHRA is allowing them to help their employees with health insurance costs for the first time, even though they aren't required by law. This is great for everyone! |

Only companies with fewer than 50 full-time employees may participate. |

Small businesses can set a budget that works for them without the fear or renewal hikes or increasing costs. |

QSEHRA cannot be offered with a group plan. |

Everyone knows benefits are super important for hiring and retaining the best talent. QSEHRA health insurance is a great way for small businesses to extend this offer to employees. |

Owner eligibility for QSEHRA depends on how your business is set up. That means in some circumstances owners are not eligible to participate in a small business HRA. |

The simplicity of QSEHRA will allow you to spend your time where it should be— focused on running your business. Since you are offering a fixed amount per month, there’s no need to spend time & mental energy trying to implement wellness programs & manage your employees’ healthcare spend to control your costs on a traditional group health plan. The right QSEHRA administration platform can make this super simple. |

There are reimbursement limits set by the IRS. Annual allowance limits go up slightly every year along with inflation. For an HRA without these limits, consider an ICHRA. |

QSEHRA allows tax-free reimbursements for premiums and qualified medical expenses (if allowed by the QSEHRA plan design). |

Premiums only and premiums + medical expenses are the only two options for reimbursement. Medical expenses only is not an option. |

Employees can shop the plan on the individual market that best meets their needs. If one employee prefers their Aetna plan, no problem. If another would like a BlueCross plan because the network includes his preferred doctors, that’s great too! |

Some areas are better for QSEHRAs than others, depending on how competitive and affordable the options are in the individual health insurance market. To see how it is in your location, check out our Qualified Small Employer HRA Heat Map tool. |

This is a big one! With QSEHRA, when a company enrolls, employees are eligible for special enrollment, which means they can shop for a major medical plan on the individual market at that time (and outside of the typical open enrollment timeframe). |

|

Unlike the individual coverage HRA, QSEHRAs can integrate with sharing ministries (if accompanied by a MEC plan), TRICARE, and spousal plan premiums. For employers, QSEHRA plans can be changed throughout the year. |

|

If an employee leaves your company, they won't lose their health plan. |

Roughly 80% of our small business clients are net new to benefits, meaning that QSEHRA is allowing them to help their employees with health insurance costs for the first time, even though they aren't required by law.

Client Spotlight: An IT Consultant Opts for QSEHRA

If your business currently has a group health plan and wants to change to a QSEHRA, you can cancel the group plan at anytime. You don’t have to wait until the end of the year or an enrollment period.

A good rule-of-thumb when determining owner eligibility is if an owner receives a W-2, he or she is likely also an employee and can participate. A W-2 isn’t fool-proof though. If you’re not sure, always verify with your licensed tax professional.

Although employees cannot contribute to a QSEHRA, employers can consider adjustments to employee base salaries to account for the reimbursement allowance. This is not recommended for most teams (it’s a bit sensitive telling employees you’re reducing their salaries) but in cases where employees are already paying for insurance out of their own pocket and the employer cannot afford to give more, we’ve seen this work. The tax savings will likely result in everyone taking home more money.

Need help designing your QSEHRA, finding a reference plan, or choosing an appropriate reimbursement rate? Chat with us! Our team can help you benchmark against similar employers in your industry as well as look at the individual market options in your location so you can save money but still offer a great, competitive benefit.

Understanding how these reimbursement options will impact your team is key to maximizing your QSEHRA’s efficiency. For instance, excluding medical expenses and premiums of spouse plans has the effect of only allowing reimbursements for employees purchasing their own insurance. This could be an effective strategy if you only need to help a few key employees or control your budget.

What happens to premium tax credits with a QSEHRA?

Rule of Thumb: In general, if your employees’ average tax credit amount is less than ~30% of the reimbursement you’re offering, QSEHRA’s pre-tax savings will still win out. If not, QSEHRA may not be a good fit for your organization. If you’re not sure, you can contact us and we’re happy to help run-the-numbers for you!

Step-by-step instructions to setup a QSEHRA

How to set up a QSEHRA

If a QSEHRA sounds like the benefit solution you need, how do you get started? Setting one up is pretty straight-forward. Here’s what you need to do:

- Design your reimbursement plan

- Create your legal plan documents

- Set a start date and cancel any group health policies (if applicable)

- Provide required notices to your employees

Step 1: Design your reimbursement plan

We covered the ins and out of reimbursement rates and requirements in the previous sections. Now it’s time to put it all together and design your reimbursement plan to achieve what you want. This is where working with an experience partner (like Take Command or, we admit, some of our competitors) can really help. Generally, we’re able to help employers come up a solution that fits their budget and needs.

Step 2: Create your legal plan documents

Do I really need plan documents or can I “just do it”?

We get asked regularly if an employer actually needs plan documents in place or if they can just administer a QSEHRA without a plan. Plan documents are not only a good idea, they are actually required. But that doesn’t mean they have to be overly complicated or expensive. Please don’t pay an attorney $1000s of dollars to draft plan documents for you. There are plenty of great off-the-shelf options. At Take Command, we set up plan documents for our clients for free.

Step 3: Set a start date and cancel any group health policies (if applicable)

Choosing a start date should be fairly easy, but there are some important timing issues employers will want to be aware of. The biggest timing factor is Open Enrollment for individual health plans which runs from November 1st to December 15th in most states. Some states have a longer Open Enrollment period but December 15th is typically the deadline for individuals to purchase a health plan that will start on January 1st of the following year.

During Open Enrollment, we recommend getting your QSEHRA setup a few weeks before the actual start date so that your employees have time to understand the benefits and choose a health plan that fits their needs. If you’re starting during the year, starting it as soon as possible will help you and your employees capture maximum tax savings.

You’ll want to include your employee notices in new employee packets and keep records that employees received the notice in a timely manner. For employers that opt to use the Take Command platform, we automatically generate these notices and keep records for you.