.jpeg?q=50&auto=format&crop=faces,entropy&fit=max&w=864&width=2880&height=1600&name=small-biz-main-hero%20(1).jpeg)

QSEHRA Reimbursement Requirements

What’s required to receive QSEHRA reimbursements?

Even though QSEHRA was brand-new in 2017, regulations governing health plans have changed significantly since then and IRS guidance has not yet caught up. You’re likely to see conflicting guidance if you search around the internet—some stuff is just out-of-date (“HRA” guidance before QSEHRA) and some of it is just wrong. We’ll do our best here to keep things up to date and will provide as many references and links to authoritative sources as we can.

QSEHRA eligibility

Here’s what is certain: You must be covered by Minimum Essential Coverage (MEC) to receive QSEHRA reimbursements. We’ll show you which plans include MEC or how to get MEC in the “Health Plans & Premiums” section below. However, for you detailed folks, MEC is defined by IRS Section 5000A(f) and the requirement to maintain it for QSEHRA is clearly spelled out in IRS Notice 2017-67, Section G. We’ve seen some employers, employees, and even some of our competitors play fast and loose with this. However, we think this can only come back to bite you. Your QSEHRA could fall apart and your employer could be hit with fines up to $100 per day per person if audited, yikes! (see Section L and IRS Section 4980D).

What happens if I don’t have MEC or I lose my MEC coverage?

Before you can ever receive a QSEHRA reimbursement, you must substantiate that you have MEC (IRS Section 9831(d)(2)(B)(ii) and IRS Notice 2017-67, Section G and Q72). This typically means providing your QSEHRA administrator with a copy of your health insurance card or other information. If you’re a Take Command member, we’ll ask you to take a photo of your card or a medical receipt to upload it online.

Once you get started, if you lose your MEC coverage for some reason, the QSEHRA reimbursements received during the time you did not have MEC will be considered taxable and you may have to pay them back (IRS Notice 2017-67 Q45 and Q62). Employers are required to stop payments immediately once they become aware an employee is not maintaining MEC or the QSEHRA itself could fall apart.

The MEC issue can be a little confusing. Make sure to check out our handy chart in the next section that breaks it down for you by plan type. If you need help, you can always contact us below!

If Take Command manages your QSEHRA, we will automatically apply pre-tax balances to your account first (to help you maximize your tax savings) and then apply any remaining balance to post-tax reimbursements (hey, it still helps!).

What types of health plans work with QSEHRA?

The great thing about QSEHRA is if you already have a health plan you love, you can probably keep it! If you need to shop for a new one, you’ll find a world of new options. Don’t worry if it feels overwhelming, we can help!

Different plan types will be treated differently under QSEHRA. You’ll want to be aware of these nuances to make sure you’re getting the most cost and tax-efficient results. Below, we’ll provide more explanation for each plan type.

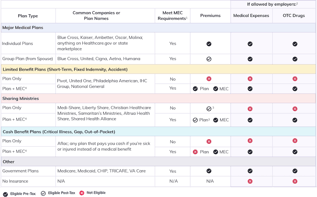

Here’s a summary table to help! You can download the table as a PDF too if you'd like.

Permitted benefits under a QSEHRA

- QSEHRA participants must maintain Minimum Essential Coverage (MEC) to receive reimbursements (IRS Notice 2017-67, Section G).

- Employers can specify whether or not to include these reimbursements under their QSEHRA rules.

- Sharing Ministries may be reimbursed post-tax outside of the QSEHRA if elected by the employer.

- Learn more about using individual MEC products to meet the MEC requirements.

Major Medical Plans

When we talk about “Major Medical” plans, we’re talking about health plans that are compliant with the Affordable Care Act (ACA). Think plans from Blue Cross, Molina, Oscar, Ambetter or other regional companies if you’re on an individual plan or United, Cigna, Aetna, etc. if you’re on your spouse’s group plan from work. Major Medical plans must:

- Insure individuals with pre-existing conditions

- Pay for preventive care at no extra cost

- Have unlimited annual and lifetime benefit levels

Because they provide all of these guaranteed benefits, Major Medical plans are typically the most expensive and only available for enrollment once per year during an Open Enrollment period (unless, of course, you have a Special Enrollment reason). If you purchased a health plan from Healthcare.gov or your state’s public marketplace, you purchased a Major Medical plan. If you get insurance from your spouse’s employer, you most likely have a Major Medical plan.

Still not sure if you have a Major Medical plan or not? Most states require insurance companies to disclose if they are not a Major Medical plan. Look for fine print that talks about exclusions, or, you can always chat with us to ask! Another giveaway—Major Medical plans must provide individuals with a 1095 each year to file with their taxes to satisfy the ACA’s individual mandate to maintain Major Medical insurance (even though that mandate is slated to go away in 2019).

If you’re covered by your spouse’s group plan there are some nuances to know regarding premium reimbursement:

- First, verify whether your employer has elected to include spouse group plans in the QSEHRA. Many will, but some won’t if they are trying to aggressively contain costs.

- Next, only the portion of the group premium that is not paid for by your spouse’s company is eligible for reimbursement. For example, let’s say your spouse’s plan costs $1,000/mo total. Your spouse’s company kicks in $400/mo to help cover the cost. Only the remaining $600 would be eligible for QSEHRA reimbursement (if allowed by the employer, see step 1 above).

- Finally, most group plans are already paid on a pre-tax basis on your spouse’s paycheck. In the example above, even though you’re paying $600/mo to cover the difference, your spouse is likely able to pay for it pre-tax on his or her paycheck. This is great! However, the IRS doesn’t want you to “double dip” and also get a pre-tax QSEHRA reimbursement. As a result, your QSEHRA claim will likely be paid on a taxable basis unless you can show the premiums were paid post-tax by your spouse (very rare). See IRS Notice 2017-67 Q48 if you’d like to dive into the weeds!

Limited Benefit Plans

Limited Benefit Plans are growing in popularity as the federal government eases regulations around them. Limited Benefit Plans do not meet the ACA’s individual mandate for everyone to have health insurance. Limited Benefit Plans are usually significantly cheaper than Major Medical plans but only provide a fixed amount of benefits (vs. unlimited benefits). Those benefits could provide great coverage, or they could be pure snake oil—the devil is in the details and fine print. Most limited plans require some level of medical underwriting and will not cover pre-existing conditions.

At Take Command, we offer a curated offering of Limited Benefit Plans to make sure our clients are getting sufficient coverage. Always, always, always….always purchase Limited Benefit Plans that have continuous coverage until the end of the calendar year—that way if you develop a condition, you can flip to a Major Medical plan during the annual open enrollment period.

A Limited Benefit Plan that pays a medical benefit will say something like “we will pay up to $1,000 a day in hospitalization benefits if you’re sick or injured”. A Cash Benefit Plan will say “we will pay you $1,000 if you get sick or injured.” One pays a doctor or hospital, one pays you cash. Subtle for sure, but important to know for QSEHRA!

To summarize: A Limited Benefit Plan alone does not work under QSEHRA. However, if you can satisfy the MEC requirement, then the Limited Benefit Plan premium is reimbursable along with Medical Expenses if allowed by the QSEHRA’s plan design.

Cash Benefit Plans

Cash Benefit Plans pay you cash if you’re sick or injured. These plans are sometimes called Critical Illness, Gap, or Out-of-Pocket plans. The most popular insurance company that writes these plans is Aflac (quack!). We rarely recommend these plans. If you read the fine print and do the math, they just typically are not a good deal for individuals and small employers. (Now, if your big company is paying for it for you…that’s a different story).

Similar to the Limited Benefit Plans above, Cash Benefit Plans by themselves do not meet the MEC requirement and are not eligible for QSEHRA reimbursement. Even if you gain access to MEC through a spouse, by purchasing an individual MEC plan, or through some other means, the Cash Benefit Plan premium will still not be eligible for reimbursement. That’s because these plans by definition do not provide a medical benefit. In IRS Publication 502, these plans fall under “Insurance Plans You Can’t Include” on page 9.

For an example of the difference between medical and cash benefits, see the previous section on “Limited Benefit Plans.”

Although the individual MEC option won’t work with Cash Benefit Plans, the MEC may still be worth it so that your Medical Expenses and OTC Drugs are reimbursable if allowed by the QSERHA’s plan design.

Sharing Ministries

Healthcare Sharing Ministries are exploding in popularity due to their lower costs and the shared values they promote. Popular Sharing Ministries include Medi-Share, Liberty Share, Christian Healthcare Ministries, Aliera, Samaritan’s Ministries, Altrua Health Share, and Shared Health Alliance among others.

The IRS has not provided much guidance on how Sharing Ministries work with QSEHRA and they really need to.

Sharing Ministry members have a special exemption under the Affordable Care Act from maintaining MEC; however, Sharing Ministries themselves do not meet the MEC requirements. We explored this circular reference in detail in this blog post.

To further complicate matters, the “premiums” you pay to be a member of a Sharing Ministry, typically referred to as a “monthly share” amount or similar, are not recognized by the IRS as being actual insurance premiums under IRS Section 213(D).

While there hasn’t been any clear guidance and it’s ultimately up to you and your tax professional, our suggestion for now is to not consider Sharing Ministries as meeting the MEC requirements and therefore not consider their monthly “premiums” as eligible for reimbursement under the QSEHRA.

But please don’t despair, there’s hope! Because Sharing Ministries are technically not insurance, they can be reimbursed on a taxable basis outside of the QSEHRA if employers want to allow it. This type of after-tax reimbursement outside of a QSEHRA is not possible for Major Medical or Limited Benefit Plans that are recognized as insurance in the eyes of the IRS because that reimbursement would constitute and Employer Payment Plan (EPP) which is subject to all sorts of group plan regulations and penalties. See this IRS guidance on “Employer Health Care Arrangements” and IRS Notice 2013-54.

But please don’t despair, there’s hope! Because Sharing Ministries are technically not insurance, they can be reimbursed on a taxable basis outside of the QSEHRA if employers want to allow it. This type of after-tax reimbursement outside of a QSEHRA is not possible for Major Medical or Limited Benefit Plans that are recognized as insurance in the eyes of the IRS because that reimbursement would constitute and Employer Payment Plan (EPP) which is subject to all sorts of group plan regulations and penalties. See this IRS guidance on “Employer Health Care Arrangements” and IRS Notice 2013-54.

On the Take Command QSEHRA Platform, we can help employers and employees track Sharing Ministry reimbursements alongside QSEHRA reimbursements for a cohesive experience. Employers have the option to turn on or off Sharing Ministry reimbursements.

If you’re being offered a QSEHRA reimbursement, you should at least consider picking up an individual MEC plan. The MEC’s premium will likely be covered by the QSEHRA reimbursement so there will be no cost to you and now you can get other medical expenses reimbursed! (if allowed by your employer)

What medical expenses can be reimbursed with QSEHRA?

The really cool thing about QSEHRA is that it’s the only vehicle that can reimburse insurance premiums and medical expenses. FSAs and HSAs can't do that! That’s awesome! It’s a great benefit because you have a ton of flexibility on how you want to spend it.

Two things must be in place before you can claim medical expense reimbursements:

- Your employer must have elected to allow medical expense reimbursement in the QSEHRA terms;

- You must meet the MEC requirements (see the section above!).

If you meet the above, you’re good to go!

QSEHRA Eligible Expenses

Have you used a Health Savings Account (HSA) or Flexible Spending Account (FSA) before? It’s the same list that governs QSEHRA (plus insurance premiums, of course). Check-out online sites like FSAStore.com to see which household products are eligible for QSEHRA (note: some items on sites like FSA store require a prescription or doctors note).

A good rule of thumb to determine if an expense is eligible or not is to ask, “Is this medically necessary or beneficial?” Doctor visits and dental cleanings = Yes. Cosmetic surgery = No. Also, you can always ask us and we can help!