We published this guide in an effort to assist business owners who are researching their options for health insurance. While we are an HRA administration company we recognize HRAs are not always the best fit, so we took our expertise with small businesses and familiarity with health insurance and produced this guide.

This guide is for employers with less than 50 employees researching health insurance for small business.

Group Health Insurance for Small Business: Know your options

When asked about health care for small business, most people envision the model of small-group insurance (sometimes referred to as “fully funded”).

That’s because it’s the model of insurance with which most people have experience. While it is the standard-bearer of employer-sponsored benefits, group health insurance for small business remains difficult to understand both for employers and employees alike.

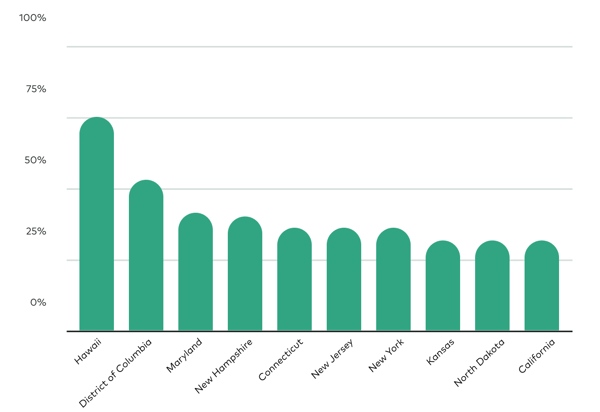

In 2018, 29.8% of employers with fewer than 50 employees offered a small group insurance plan to at least some of their employees.

Data from The Kaiser Family Foundation reveals that employers in Hawaii were the highest contributors (74.9%), while employers in Utah were the lowest contributors (17.5%).

NOTE: Hawaii's Prepaid Health Care Act (or PHCA) accounts for the high percentage of coverage.

How does small-group insurance work?

The process typically begins with a conversation with a small business health insurance broker—although a broker is not absolutely necessary.

What are small business health insurance brokers?

Small business health insurance brokers are the go-between for employers and insurance companies (also called “underwriters” or “carriers”), and they are the ones who do most of the upfront work in finding a plan for employers.

Typically, brokers will collect a company’s employee information into one document (called a “census”) and use that to begin finding the ideal plan for their clients.

Census information usually includes: name, age, date of birth, number of dependents, and zip code.

The broker (or sometimes, the employer) will submit the employee census to various carriers and begin the process of collecting multiple quotes.

It’s worth noting that brokers will not be able to negotiate better pricing with carriers.

This is because the insurance plan premiums (aka “rates”) are filed with and approved by the state-level Department of Insurance on an annual or quarterly basis.

Do I need a small business insurance broker?

The real value with small business insurance brokers is their streamlined ability to collect quotes based on the employee census as well as creating a bundle of ancillary products that add value to all employees (i.e. dental, vision, FSA, HSA, etc.). By law, brokers are not permitted to mark-up pricing on group plans.

A good small business insurance broker will help educate a client and explore possible solutions to providing benefits to their staff. Small business health insurance brokers provide employers peace of mind and industry experience.

Brokers do not, however, provide unique proprietary insurance products that are unavailable elsewhere.

It’s worth noting that many brokers’ primary income comes from making a commission (or “finder’s fee”) from the insurance company the employer selects. This fee is typically based on the number of employees that enroll in the selected plan (or a percentage of premiums paid) and is typically built into the cost of the group plan.

About the Small Business Health Options Program

If an employer chooses to search for a small group plan on their own, they can use Healthcare.gov’s Small Business Options Program (SHOP) Marketplace, locate a private exchange, or search directly with the various carriers.

Once a small business insurance company reviews the employee census, they will determine the risk associated with that particular small business health insurance company and create an appropriate cost for underwriting the company.

What this means is the small business insurance company will take into account all of the employees and their projected/expected health needs and risks for the up-and-coming plan year and establish a dollar amount (or “fixed premium”) for the employees to offset the risk they are about to inherit.

The Affordable Care Act (ACA) and prior state-specific regulations created what’s called “community rating” for small group health plans.

This means that while carriers in most states can vary premiums by age and location, the health status of individual employees has no bearing on the cost of the health insurance plans. Insurance companies cannot charge a small business client more or less because their employees are either sick or healthy.

The "employer contribution" is the portion of the employee's fixed premium that the employer chooses to cover.

Once the broker has collected quotes for the employer (the number of options presented as well as types of “bundled” ancillary products will vary depending on each broker), they will present the options and typically make recommendations based on the company’s needs.

Employers then select the insurance carrier and plan design option(s) they will offer employees.

Once a plan is selected, the employer determines how much of the fixed premium they want to cover (also known as the “employer contribution”) and while each employer’s contribution varies based on their location and preferred carrier, most states require that businesses contribute at least 50% of the total fixed premium for each employee.

About the Small Business Health Care Tax Credit

Some small employers may qualify for the Small Business Health Care Tax Credit which helps businesses (less than 25 employees) offset the cost of their contributions up to 50 percent if they use the SHOP.

According to The Kaiser Family Foundation, in 2019 small business employers contributed on average 71% of the premiums for their employees with family coverage and 83% for employees with single coverage.

In fact, for single coverage employees, small employers covered 100% of the premium for 31% of all employees while 35% of employees received less than half.

Employer Contributions |

|

|

|

Family Coverage (71%) |

Single Coverage (83%) |

Employer Health Insurance Costs: What to Expect

Every year, community-rated premiums are recalculated based on the previous year’s usage and the carriers’ projections for the up-and-coming year.

While not always the case, premium rates often increase year over year. In 2019, group health insurance rates outpaced both inflation and worker’s salary increases.

The average premium for single coverage for 2019 was 4% higher than the previous year, and the average premium for family coverage was 5% higher as well according to The Kaiser Family Foundation.

Over the past five years, small businesses saw an estimated 28% increase in annual family premiums.

Once a plan is selected, the employer typically holds a meeting to present the plan to the employees and begins the process of getting them enrolled.

If a broker is involved, this process is oftentimes handled by the broker.

Small-group plans require participation rates in order to effectively manage the risk. As an example, Healthcare.gov’s SHOP requires a 70% participation rate in order to honor the quoted fixed premium.

What is self-funded health insurance?

Self-funded health insurance is a type of self-insurance where the business pays for its employees’ medical expenses with its own funds rather than leveraging an insurance carrier.

In this manner, the company is assuming all the health risk instead of an underwriter and therefore, this type of insurance is most often used by large employers with plenty of cashflow to handle the totality of the incoming employee claims and mitigate the potential risk.

Self-funded health insurance is oftentimes used by larger companies with dedicated staff and wellness programs in place.

While not uncommon with small employers, the vast majority of employers opting for this option are large/enterprise-level companies.

In fact, 81% of covered employees who work for a company with more than 200 employees were part of a self-funded plan.

Only 13% of covered employees at companies with 3 to 199 employees were part of a self-funded plan.

Self-Funded Health Insurance |

|

|

|

200+ Employees (81%) |

3 to 199 Employees (13%) |

How Many Employees Do You Need Before You Must Provide Health Insurance?

Under the Affordable Care Act (ACA), businesses must provide health insurance if they have 50 or more full-time equivalent (FTE) employees. This mandate is part of what's known as the Employer Shared Responsibility Provision. Companies falling under this requirement must offer affordable health insurance and minimum value to their full-time employees and their children up to age 26, or they may face a penalty. Providing health insurance is optional for businesses with fewer than 50 FTE employees. It comes with certain flexibilities and incentives, such as offering a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) or participating in the Small Business Health Options Program (SHOP).

Do Small Businesses Pay More for Health Insurance for Their Employees?

Small businesses often face higher per-employee health insurance costs than larger companies. This discrepancy is primarily due to small businesses' smaller risk pool, administrative fees, and lack of bargaining power in the health insurance market. Insurers often charge higher premiums for small groups because the risk is spread across a smaller number of individuals, which can result in more significant variability in healthcare usage and costs.

However, there are ways for small businesses to manage these costs and still provide valuable health benefits to their employees. Exploring alternative health benefit options such as HRAs (like QSEHRA and ICHRA), participating in SHOP, or joining a professional employer organization (PEO) that offers access to more extensive group insurance plans can help mitigate some of these costs. Additionally, tax credits and incentives are available for certain small businesses that provide health insurance to their employees, helping lower the overall expense.

How does self-funded insurance work?

Initially, an employer will work with a TPA ( or “Third-Party Administrator”) to manage the creation of plan documents, assist with claims adjudication, and handle payments.

TPAs are only partially necessary (or legally required), but employers will need adequately trained staff to dedicate time and energy otherwise.

In 2018, only 8% of companies with 3 to 49 employees took advantage of a self-funded plan. [source: Kaiser Family Foundation]

Learn more: Is level-funded a good fit?

In terms of plan design, level-funded plans work similarly to self-funded plans with regards to flexibility and customization. Employees typically experience a high degree of choices and options under these plans.

Over one-third (34%) of the small employers we've had conversations with over the last two years did not previously offer a formal benefits solution.

This list is not comprehensive. Each employer should continue to research options and speak with professionals before moving forward.

.jpeg?q=50&auto=format&crop=faces,entropy&fit=max&w=600&width=600&height=400&name=ichraprosandcons%20(1).jpeg)

Read: Employer Health Benefits - 2019 Summary of Findings

The Affordable Care Act (ACA), also known as Obamacare, standardized individual and small-group insurance plans into the metal tier system to make it easier for consumers to compare plans. Click here to learn more about coverage options.

Carrier Selection

Because all carriers price their products differently based on several variables, similar coverage will vary greatly from one carrier to another.

Aside from fixed costs like overhead and internal budgetary expenses, carriers also must align pricing based on contractual agreements with entities like doctors, hospital networks, and drug manufacturers.

Employer Contribution

While the average cost of insurance per employees in 2019 was $599/mo, that doesn’t mean the employer is responsible for paying that entire amount.

During the process of securing benefits, employers will make a determination on how much they’d like to contribute towards the employees’ monthly premium.

While most states require employers to cover at least 50% of the premium, the final decision is up to the employers.

An average of 71% of the premiums for families and 83% for single employees were covered by employers in 2019.

Employer Contributions |

|

|

|

Family Coverage (71%) |

Single Coverage (83%) |

How much does self-funded/level-funded health insurance cost?

Self-funded (and level-funded) health insurance have both predictable, fixed costs as well as unpredictable, variable costs.

Self-funded (and level-funded) health insurance have both predictable, fixed costs as well as unpredictable, variable costs.

The fixed costs that come with a self-funding option include administration fees and stop-loss insurance. The cost of these items will vary depending on the partners selected to handle each task, but their costs for the year will be predictable.

The largest factor in determining the cost for self-funded insurance will be the annual claims total from the employees—the total of the employees’ health care spend over the course of the previous year.

- TPA fees: TPA fees will vary greatly depending on the services performed as well as which partner is selected. Additionally, how they structure their pricing will vary. Some TPAs will charge a flat overall rate for administration while other companies will charge a price per employee participating in the plan. The fee can also vary if employee benefit services are offered by various TPA branches or outsourced to specialists.

- Stop-loss insurance: According to Aegis Risk, the average cost for stop-loss insurance premiums in 2019 ranged from around $25/mo to $142/mo depending on the desired deductible.

- Variable Claims: The total sum of healthcare cost from all the employees in a given year will greatly vary depending on the health and well-being of the employees.

How much does an HRA cost?

The primary cost associated with offering an HRA as a health benefit is the predetermined reimbursement rates established by the employer.

Additionally, there could be setup fees and on-going administration fees if the employer decides to outsource the administration to another company.

If an employer chooses to self-administer their HRA there will be no administration fees, but there will typically be fees associated with producing the initial plan document for the IRS.

Take Command offers HRAs with no set up fees or long term contracts. Plan documents are always included at no additional cost.

HRA Administrators vary widely from CPAs offering bare minimum services on the side to benefits companies offering HRAs as one of many options to HRA administrators exclusively specializing in HRA management.

Employers should consult with a tax or benefits professional to fully understand the legal requirements for each situation.