The Individual Coverage Health Reimbursement Arrangement (ICHRA) is just over one-year old and steadily gaining in popularity as a benefits solution for employers. ICHRA allows employers to establish a tax-free reimbursement for employees and allows employees to pick an individual health plan that meets their needs. Employers love the predictability and employees love the choice: win-win. So which carriers are ready for this trend to continue to grow and which states have a leg up?

ICHRA is projected to grow significantly over the next few years and presents a great opportunity for insurance companies to expand coverage. The government projects approximately 10M employees will be covered by an ICHRA through their employer in the next 5-10 years.

A recent study by KFF and PBGH revealed that 48% of its respondents said they were "considerably or highly likely" to use an ICHRA to offer alternative coverage to employees.

At Take Command, we’ve found that over 70% of our small employers moving to ICHRA are offering benefits for the first time—so ICHRA has a chance to cover more lives than before.

So how can insurance companies prepare for ICHRA? And which insurance companies are positioned to win in their market?

More than anything carriers need to be prepared to make operational adjustments to prepare for ICHRA.

ICHRA rules prevent private exchanges from limiting which plans are shown to employees during the shopping process, but insurance companies can stand out (or get left behind) based on four operational criteria:

- Do you appoint remote brokers? While ICHRA is inherently simple to understand, meeting the requirements takes expertise from an experienced broker or consultant that make revenue through commissions. In addition, employees used to group plans are used to being supported by brokers when they need help with their plan, replacing a lost card, etc and don’t want to call an insurance company directly.

- Do you accept electronic bulk enrollment files? Brokers and private exchanges supporting ICHRA need a way to efficiently enroll hundreds of employees at once. In most cases, the broker or exchange will have all of the information they need to complete enrollment for an employee after receiving the employee’s plan choice.

- Can brokers or private exchanges provide payment information (binder and recurring) for employees? Similar to above, private exchanges are coming up with unique payment solutions that enable ICHRA to look and function similar to a traditional group plan. Brokers and exchanges need to be able to provide payment information on behalf of employees.

- Do you offer off-exchange plans? Employees that choose a plan that costs more than their allowance will have to put in some of their own money to cover the difference. That difference can be tax-free when combined with a Section 125 payroll deduction but only for off-exchange plans (due to some ACA restrictions).

How do these operational things add up to influence an employee’s shopping decision?

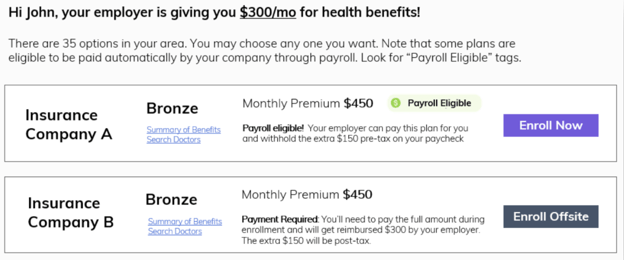

Let’s look at an example. Below is a fictitious “screen shot” from a private exchange supporting an ICHRA enrollment. In this scenario, an employee named John is being provided $300/mo by his employer to choose a health plan.

There are 35 plans in his area; a private exchange will have to show all of those options so pretend the screen scrolls down to list all of the options. In this case, John is choosing between two finalists—Bronze plans with similar price points and plan features from Insurance Companies A and B: Although the plans are very similar, Company A has taken the operational steps listed above and Company B has not.

What does this mean for John? A LOT! If John chooses the plan from Company A, he’s essentially done. The private exchange (and the broker) have the information needed to complete the enrollment for John and his family. The unreimbursed portion of the premium ($150 in this example) will be withheld on John’s paycheck tax-free and the entire amount will be paid to Company A by the employer on John’s behalf.

If John chooses the plan from Company B, he’ll have to complete enrollment on Company B’s website or through a state exchange. He will then have to provide proof of enrollment back to the entity managing the ICHRA (usually a screen shot or a receipt). John will have to provide his personal payment information to Company B and make his binder and recurring payments each month on his own—floating the cost until he is reimbursed by the ICHRA administrator.

In addition, the $150 unreimbursed portion of the premium comes out of John’s taxable income. It’s easy to see how Insurance Company A will get the lion’s share of enrollments compared to Company B because they were operationally ready for ICHRA.

From our experience at Take Command, our enrollment team saw employees willing to pay more to have convenience over known brand names, etc.

We haven’t even talked about plan designs and features yet which will also be important, but won’t matter to employees if they have to jump through hoops to enroll.

So which insurance companies are operationally ready for ICHRA?

In the table below, we summarize the ICHRA Operational Readiness for insurance companies based on our review of their current capabilities. We list insurance companies by state so they can think about two primary strategies:

- Offense: Some insurance companies have the opportunity to be “first movers” for ICHRA in their state and position themselves to win an outsized share of the ICHRA market.

- Defense: Some insurance companies will need to play catch up so they don’t lose additional market share to employers switching to the ICHRA model.

| State | Insurance Company | ICHRA Readiness | Appoint Remote Brokers | Bulk Enrollment | Payment Information | Off-Exchange Plans Offered |

| AK | Moda Health | 0% | No | No | No | No |

| AK | Premera BCBS of Alaska | 50% | Yes | No | No | Yes |

| AL | BCBS AL | 50% | No | No | Yes | Yes |

| AL | Bright Health Plan | 75% | Yes | No | Yes | Yes |

| AR | Ambetter | 100% | Yes | Yes | Yes | Yes |

| AR | Arkansas BCBS | 50% | No | No | Yes | Yes |

| AR | QualChoice | 50% | No | No | Yes | Yes |

| AZ | Ambetter | 100% | Yes | Yes | Yes | Yes |

| AZ | BCBS AZ | 75% | Yes | No | Yes | Yes |

| AZ | Bright Health Plan | 75% | Yes | No | Yes | Yes |

| AZ | Cigna | 75% | Yes | No | Yes | Yes |

| AZ | Oscar | 75% | Yes | No | Yes | Yes |

| AZ | United Healthcare | 0% | No | No | No | No |

| CA | Anthem | 75% | Yes | No | Yes | Yes |

| CA | BlueShield of California | 75% | Yes | No | Yes | Yes |

| CA | Chinese Community Health | 25% | No | No | Yes | No |

| CA | Health Net | 100% | Yes | Yes | Yes | Yes |

| CA | Kaiser Permanente | 75% | Yes | No | Yes | Yes |

| CA | L.A. Care Health Plan | 50% | Yes | No | Yes | No |

| CA | Molina | 50% | Yes | No | Yes | No |

| CA | Oscar | 75% | Yes | No | Yes | Yes |

| CA | Sharp Health Plan | 50% | Yes | No | No | Yes |

| CA | Sutter Health Plan | 25% | Yes | No | No | Yes |

| CA | Valley Health Plan | 50% | Yes | No | Yes | No |

| CA | Western Health Advantage | 50% | Yes | No | No | Yes |

| CO | Anthem | 75% | Yes | No | Yes | Yes |

| CO | Bright Health Plan | 75% | Yes | No | Yes | Yes |

| CO | Cigna | 75% | Yes | No | Yes | Yes |

| CO | Denver Health Medical Plan | 25% | No | No | No | Yes |

| CO | Friday Health Plan | 75% | Yes | No | Yes | Yes |

| CO | Kaiser Permanente | 75% | Yes | No | Yes | Yes |

| CO | Oscar | 75% | Yes | No | Yes | Yes |

| CO | Rocky Mountain Health Plans | 75% | Yes | No | Yes | Yes |

| CT | Anthem | 75% | Yes | No | Yes | Yes |

| CT | ConnectiCare | 75% | Yes | No | Yes | Yes |

| DC | CareFirst BCBS | 25% | Yes | No | No | No |

| DC | Kaiser Permanente | 25% | Yes | No | No | No |

| DE | Highmark BCBS | 50% | Yes | No | No | Yes |

| FL | Ambetter | 100% | Yes | Yes | Yes | Yes |

| FL | AvMed | 75% | Yes | No | Yes | Yes |

| FL | Bright Health Plan | 75% | Yes | No | Yes | Yes |

| FL | Cigna | 75% | Yes | No | Yes | Yes |

| FL | Florida Blue | 25% | No | No | No | Yes |

| FL | Florida Health Care Plans | 25% | No | No | No | Yes |

| FL | Health First Health Plans | 75% | Yes | No | Yes | Yes |

| FL | Molina | 50% | Yes | No | Yes | No |

| FL | Oscar | 75% | Yes | No | Yes | Yes |

| GA | Alliant Health Plans | 75% | Yes | No | Yes | Yes |

| GA | Ambetter | 100% | Yes | Yes | Yes | Yes |

| GA | Anthem | 75% | Yes | No | Yes | Yes |

| GA | CareSource Just4Me | 25% | Yes | No | No | No |

| GA | Kaiser Permanente | 75% | Yes | No | Yes | Yes |

| GA | Oscar | 75% | Yes | No | Yes | Yes |

| HI | Kaiser Permanente | 50% | Yes | No | Yes | Yes |

| HI | HMSA | 0% | No | No | No | No |

| IA | Medica Insurance Company | 75% | Yes | No | Yes | Yes |

| IA | Oscar | 75% | Yes | No | Yes | Yes |

| IA | Wellmark BCBS of Iowa | 0% | No | No | No | No |

| ID | BlueCross of Idaho | 50% | No | No | Yes | Yes |

| ID | Mountain Health CO-OP | 75% | Yes | No | Yes | Yes |

| ID | PacificSource Health Plans | 50% | No | No | Yes | Yes |

| ID | Regence BlueShield of Idaho | 75% | Yes | No | Yes | Yes |

| ID | SelectHealth | 50% | No | No | Yes | Yes |

| IL | Ambetter | 100% | Yes | Yes | Yes | Yes |

| IL | BCBS Illinois | 75% | Yes | No | Yes | Yes |

| IL | Bright Health Plan | 75% | Yes | No | Yes | Yes |

| IL | Cigna | 75% | Yes | No | Yes | Yes |

| IL | Health Alliance | 75% | Yes | No | Yes | Yes |

| IL | MercyCare Health Plans | 50% | No | No | Yes | Yes |

| IL | Quartz | 50% | No | No | Yes | Yes |

| IL | WellFirst Health | 25% | No | No | Yes | No |

| IN | Ambetter | 100% | Yes | Yes | Yes | Yes |

| IN | Anthem | 75% | Yes | No | Yes | Yes |

| IN | CareSource Just4Me | 25% | Yes | No | No | No |

| KS | Ambetter | 100% | Yes | Yes | Yes | Yes |

| KS | BCBS of Kansas | 50% | No | No | Yes | Yes |

| KS | BlueKC | 25% | Yes | No | No | No |

| KS | Cigna | 75% | Yes | No | Yes | Yes |

| KS | Medica Insurance Company | 75% | Yes | No | Yes | Yes |

| KS | Oscar | 75% | Yes | No | Yes | Yes |

| KY | Anthem | 75% | Yes | No | Yes | Yes |

| KY | CareSource Just4Me | 25% | Yes | No | No | No |

| LA | BCBS of Louisiana | 50% | No | No | Yes | Yes |

| LA | CHRISTUS Health Plan | 25% | Yes | No | No | No |

| LA | Vantage Health | 0% | No | No | No | No |

| MA | AllWays Health Partners (aka Neighborhood Health Plan) | 25% | No | No | Yes | No |

| MA | BMC HealthNet | 25% | No | No | Yes | No |

| MA | BCBS of Massachusetts | 50% | No | No | Yes | Yes |

| MA | Fallon Health | 50% | Yes | No | Yes | No |

| MA | Harvard Pilgrim | 50% | Yes | No | No | Yes |

| MA | Health New England | 25% | No | No | Yes | No |

| MA | Tufts Health Plans | 25% | No | No | Yes | No |

| MA | United Healthcare | 25% | No | No | Yes | No |

| MD | CareFirst BCBS | 50% | Yes | No | No | Yes |

| MD | Kaiser Permanente | 75% | Yes | No | Yes | Yes |

| MD | United Healthcare | 25% | No | No | No | Yes |

| ME | Anthem | 50% | Yes | No | Yes | Yes |

| ME | Community Health Options | 25% | No | No | No | Yes |

| ME | Harvard Pilgrim | 50% | Yes | No | No | Yes |

| MI | Ambetter | 100% | Yes | Yes | Yes | Yes |

| MI | BCBS Michigan | 75% | Yes | No | Yes | Yes |

| MI | HAP | 75% | Yes | No | Yes | Yes |

| MI | McLaren Health Plan | 25% | Yes | No | No | No |

| MI | Meridian Choice | 0% | No | No | No | No |

| MI | Molina | 25% | Yes | No | No | No |

| MI | Oscar | 75% | Yes | No | Yes | Yes |

| MI | Physicians Health Plan | 75% | Yes | No | Yes | Yes |

| MI | Priority Health Plan | 75% | Yes | No | Yes | Yes |

| MI | Total Health Care USA | 75% | Yes | No | Yes | Yes |

| MN | BCBS Minnesota | 75% | Yes | No | Yes | Yes |

| MN | HealthPartners | 25% | No | No | No | Yes |

| MN | Medica Insurance Company | 75% | Yes | No | Yes | Yes |

| MN | PreferredOne | 75% | Yes | No | Yes | Yes |

| MN | Quartz | 50% | No | No | No | Yes |

| MN | UCare | 0% | No | No | No | No |

| MO | Ambetter | 50% | Yes | No | Yes | No |

| MO | Anthem | 75% | Yes | No | Yes | Yes |

| MO | Cigna | 75% | Yes | No | Yes | Yes |

| MO | Cox Health Systems Insurance Company | 0% | No | No | No | No |

| MO | Medica Insurance Company | 75% | Yes | No | Yes | Yes |

| MO | Oscar | 75% | Yes | No | Yes | Yes |

| MO | SSM Health Insurance Company | 0% | No | No | No | No |

| MS | Ambetter | 25% | Yes | No | No | No |

| MS | Molina | 25% | Yes | No | No | No |

| MT | BCBS Montana | 75% | Yes | No | Yes | Yes |

| MT | Montana Health CO-OP | 75% | Yes | No | Yes | Yes |

| MT | PacificSource Health Plans | 50% | No | No | Yes | Yes |

| NC | Ambetter | 25% | Yes | No | No | No |

| NC | BCBS North Carolina | 50% | No | No | Yes | Yes |

| NC | Bright Health Plan | 75% | Yes | No | Yes | Yes |

| NC | Cigna | 75% | Yes | No | Yes | Yes |

| NC | Oscar | 75% | Yes | No | Yes | Yes |

| NC | United Healthcare | 25% | No | No | No | Yes |

| ND | BCBS North Dakota | 50% | No | No | Yes | Yes |

| ND | Medica Insurance Company | 75% | Yes | No | Yes | Yes |

| ND | Sanford Health Plan | 50% | No | No | Yes | Yes |

| NE | Bright Health Plan | 75% | Yes | No | Yes | Yes |

| NE | Medica Insurance Company | 75% | Yes | No | Yes | Yes |

| NH | Ambetter | 100% | Yes | Yes | Yes | Yes |

| NH | Anthem | 75% | Yes | No | Yes | Yes |

| NH | Harvard Pilgrim | 50% | Yes | No | No | Yes |

| NJ | AmeriHealth | 75% | Yes | No | Yes | Yes |

| NJ | Horizon BCBS of New Jersey | 75% | Yes | No | Yes | Yes |

| NJ | Oscar | 75% | Yes | No | Yes | Yes |

| NJ | Oxford | 25% | No | No | No | Yes |

| NM | Ambetter | 25% | Yes | No | No | No |

| NM | BCBS New Mexico | 75% | Yes | No | Yes | Yes |

| NM | Friday Health Plan | 75% | Yes | No | Yes | Yes |

| NM | Molina | 25% | Yes | No | No | No |

| NM | Presbyterian Health Plan | 75% | Yes | No | Yes | Yes |

| NM | True Health New Mexico | 75% | Yes | No | Yes | Yes |

| NV | Ambetter | 25% | Yes | No | No | No |

| NV | Anthem | 75% | Yes | No | Yes | Yes |

| NV | Friday Health Plan | 75% | Yes | No | Yes | Yes |

| NV | Health Plan of Nevada | 25% | No | No | No | Yes |

| NV | Hometown Health | 50% | No | No | Yes | Yes |

| NV | SelectHealth | 50% | No | No | Yes | Yes |

| NV | Sierra Health and Life | 50% | No | No | Yes | Yes |

| NY | Aetna | 0% | No | No | No | No |

| NY | BCBS of Western New York | 50% | No | No | Yes | Yes |

| NY | BlueShield of Northeastern New York | 50% | No | No | Yes | Yes |

| NY | CDPHP | 50% | No | No | Yes | Yes |

| NY | EmblemHealth | 50% | No | No | Yes | Yes |

| NY | Empire BCBS | 0% | No | No | No | No |

| NY | Excellus | 50% | No | No | Yes | Yes |

| NY | Fidelis Care | 0% | No | No | No | No |

| NY | HealthFirst | 0% | No | No | No | No |

| NY | Independent Health | 50% | No | No | Yes | Yes |

| NY | MVP Health Plans | 50% | No | No | Yes | Yes |

| NY | MetroPlus Health Plan | 0% | No | No | No | No |

| NY | Oscar | 75% | Yes | No | Yes | Yes |

| NY | United Healthcare | 0% | No | No | No | No |

| OH | Ambetter | 100% | Yes | Yes | Yes | Yes |

| OH | Anthem | 75% | Yes | No | Yes | Yes |

| OH | AultCare Insurance | 25% | Yes | No | No | No |

| OH | CareSource Just4Me | 25% | Yes | No | No | No |

| OH | Medical Mutual | 25% | Yes | No | No | No |

| OH | Molina | 25% | Yes | No | No | No |

| OH | Oscar | 75% | Yes | No | Yes | Yes |

| OH | Paramount Insurance | 0% | No | No | No | No |

| OH | SummaCare | 75% | Yes | No | Yes | Yes |

| OK | BCBS Oklahoma | 75% | Yes | No | Yes | Yes |

| OK | Bright Health Plan | 75% | Yes | No | Yes | Yes |

| OK | CommunityCare | 25% | No | No | No | Yes |

| OK | Medica | 75% | Yes | No | Yes | Yes |

| OK | Oscar | 75% | Yes | No | Yes | Yes |

| OK | United Healthcare | 0% | No | No | No | No |

| OR | BridgeSpan Health Company | 75% | Yes | No | Yes | Yes |

| OR | Kaiser Permanente | 75% | Yes | No | Yes | Yes |

| OR | Moda Health | 50% | No | No | Yes | Yes |

| OR | PacificSource Health Plans | 50% | No | No | Yes | Yes |

| OR | Providence Health Plan | 50% | No | No | Yes | Yes |

| OR | Regence BCBS | 75% | Yes | No | Yes | Yes |

| PA | Ambetter | 100% | Yes | Yes | Yes | Yes |

| PA | Capital Blue Cross | 75% | Yes | No | Yes | Yes |

| PA | Geisinger | 0% | No | No | No | No |

| PA | Highmark BCBS | 50% | Yes | No | No | Yes |

| PA | Independence Blue Cross | 75% | Yes | No | Yes | Yes |

| PA | Oscar | 75% | Yes | No | Yes | Yes |

| PA | UPMC | 75% | Yes | No | Yes | Yes |

| RI | BCBS Rhode Island | 75% | Yes | No | Yes | Yes |

| RI | Neighborhood Health Plan of Rhode Island | 50% | No | No | Yes | Yes |

| SC | Ambetter | 25% | Yes | No | No | No |

| SC | BlueChoice Health Plan of South Carolina | 75% | Yes | No | Yes | Yes |

| SC | BCBS South Carolina | 75% | Yes | No | Yes | Yes |

| SC | Bright Health Plan | 75% | Yes | No | Yes | Yes |

| SC | Molina | 50% | Yes | No | Yes | No |

| SD | Avera Health Plans | 50% | No | No | Yes | Yes |

| SD | Sanford Health Plan | 50% | No | No | Yes | Yes |

| TN | Ambetter | 25% | Yes | No | No | No |

| TN | BCBS Tennessee | 75% | Yes | No | Yes | Yes |

| TN | Bright Health Plan | 75% | Yes | No | Yes | Yes |

| TN | Cigna | 75% | Yes | No | Yes | Yes |

| TN | Oscar | 75% | Yes | No | Yes | Yes |

| TN | United Healthcare | 0% | No | No | No | No |

| TX | Ambetter | 100% | Yes | Yes | Yes | Yes |

| TX | BCBS Texas | 75% | Yes | No | Yes | Yes |

| TX | CHRISTUS Health Plan | 50% | Yes | No | No | Yes |

| TX | Community Health Choice | 0% | No | No | No | No |

| TX | El Paso First Health Plans | 0% | No | No | No | No |

| TX | Firstcare Health Plans | 0% | No | No | No | No |

| TX | Friday Health Plans | 75% | Yes | No | Yes | Yes |

| TX | Molina | 25% | Yes | No | No | No |

| TX | Oscar | 75% | Yes | No | Yes | Yes |

| TX | Scott & White | 75% | Yes | No | Yes | Yes |

| TX | Sendero Health Plans | 0% | No | No | No | No |

| UT | BridgeSpan Health Company | 75% | Yes | No | Yes | Yes |

| UT | Cigna | 75% | Yes | No | Yes | Yes |

| UT | Molina | 25% | Yes | No | No | No |

| UT | Regence BCBS | 75% | Yes | No | Yes | Yes |

| UT | SelectHealth | 50% | No | No | Yes | Yes |

| UT | University of Utah Health Plan | 75% | Yes | No | Yes | Yes |

| VA | Anthem | 75% | Yes | No | Yes | Yes |

| VA | CareFirst BCBS | 50% | Yes | No | No | Yes |

| VA | Cigna | 75% | Yes | No | Yes | Yes |

| VA | Kaiser Permanente | 75% | Yes | No | Yes | Yes |

| VA | Optima Health | 75% | Yes | No | Yes | Yes |

| VA | Oscar | 75% | Yes | No | Yes | Yes |

| VA | Piedmont Healthcare | 0% | No | No | No | No |

| VA | United Healthcare | 50% | No | No | Yes | Yes |

| VT | BCBS Vermont | 50% | No | No | Yes | Yes |

| VT | MVP Health Plans | 50% | No | No | Yes | Yes |

| WA | Ambetter | 25% | Yes | No | No | No |

| WA | Asuris Northwest Health | 75% | Yes | No | Yes | Yes |

| WA | BridgeSpan Health Company | 75% | Yes | No | Yes | Yes |

| WA | Community Health Network of Washington | 0% | No | No | No | No |

| WA | Health Alliance | 50% | No | No | Yes | Yes |

| WA | Kaiser Permanente | 75% | Yes | No | Yes | Yes |

| WA | LifeWise Health Plan | 50% | No | No | Yes | Yes |

| WA | Molina | 25% | Yes | No | No | No |

| WA | PacificSource Health Plans | 50% | No | No | Yes | Yes |

| WA | Premera Blue Cross | 75% | Yes | No | Yes | Yes |

| WA | Providence Health Plan | 50% | No | No | Yes | Yes |

| WA | Regence BCBS | 75% | Yes | No | Yes | Yes |

| WA | Regence BlueShield | 75% | Yes | No | Yes | Yes |

| WA | United Healthcare | 0% | No | No | No | No |

| WI | Anthem | 75% | Yes | No | Yes | Yes |

| WI | Aspirus Arise Health Plan of Wisconsin | 75% | Yes | No | Yes | Yes |

| WI | Arise Health Plan | 75% | Yes | No | Yes | Yes |

| WI | Common Ground Healthcare Cooperative | 75% | Yes | No | Yes | Yes |

| WI | Dean Health Plan | 25% | Yes | No | No | No |

| WI | Group Health Cooperative | 50% | No | No | Yes | Yes |

| WI | Health Partners | 50% | No | No | Yes | Yes |

| WI | Medica Insurance Company | 75% | Yes | No | Yes | Yes |

| WI | MercyCare Health Plans | 50% | No | No | Yes | Yes |

| WI | Molina | 25% | Yes | No | No | No |

| WI | Network Health Plan | 75% | Yes | No | Yes | Yes |

| WI | Quartz | 50% | No | No | Yes | Yes |

| WI | Security Health Plan | 75% | Yes | No | Yes | Yes |

| WI | Together with Children's Community Health Plan | 75% | Yes | No | Yes | Yes |

| WI | Wisconsin Physicians SVC Insurance Corp | 75% | Yes | No | Yes | Yes |

| WV | CareSource Just4Me | 25% | Yes | No | No | No |

| WV | Highmark BCBS | 50% | Yes | No | No | Yes |

| WY | BCBS Wyoming | 50% | No | No | Yes | Yes |

| WY | Mountain Health CO-OP | 50% | No | No | Yes | Yes |

Which states are ready for ICHRA from a carrier preparedness standpoint?

We've put together a chart to demonstrate which states are positioned to win with ICHRA based on their carriers' level of readiness.

| State | Overall ICHRA Readiness |

| AK | 25% |

| AL | 62.5% |

| AR | 50% |

| AZ | 66.7% |

| CA | 58.3% |

| CO | 68.75% |

| CT | 75% |

| DC | 25% |

| DE | 50% |

| FL | 63.8% |

| GA | 70.8% |

| HI | 25% |

| IA | 50% |

| ID | 60% |

| IL | 53.13% |

| IN | 66.7% |

| KS | 66.67% |

| KY | 50% |

| LA | 25% |

| MA | 34% |

| MD | 50% |

| ME | 41.67% |

| MI | 60% |

| MN | 45.83% |

| MO | 50% |

| MS | 25% |

| MT | 66.67% |

| NC | 65% |

| ND | 58.33% |

| NE | 75% |

| NH | 75% |

| NJ | 62.50% |

| NM | 58.33% |

| NV | 50% |

| NY | 30.36% |

| OH | 47.22% |

| OK | 66.67% |

| OR | 62.5% |

| PA | 64.2% |

| RI | 62.5% |

| SC | 60% |

| SD | 50% |

| TN | 54.16% |

| TX | 43.18% |

| UT | 62.5% |

| VA | 59.38% |

| VT | 50% |

| WA | 50% |

| WI | 61.67% |

| WV | 37.5% |

| WY | 62.5% |

See something not right? Want to learn how you can implement these changes?

We'd love to talk to you about ICHRA preparedness! Contact Emily@TakeCommandHealth.com and Mackenzie@TakeCommandHealth.com.

Last updated: 7/15/21