Fringe Benefits

Health & Wellness

By promoting healthy lifestyles for employees and their families, you are helping them lead happier lives.

- Fitness Reimbursements

- Discount Card Programs (Fresh Bennies)

- Telehealth (Teledocs, etc.)

- Mental Health Assistance (Better Help, Etc.)

- Headspace/Calm Subscription

- Wellness Challenges (Steps challenge, walkathon, healthy cooking class, Etc.)

Gary was diagnosed with pre-diabetes. Afraid of his health, Gary decided to make some lifestyle changes. He took advantage of his employee’s Fitness Reimbursement program and got a membership to a local gym. Through exercise and nutrition coaching, Gary lost 50 pounds and lowered his blood sugar levels to a normal range.

I feel better than ever! Not only did I lose weight and get my body in shape, my anxiety is gone too. I feel both physically and mentally strong.

- Gary

Sharice noticed she was more anxious than normal and was feeling overwhelmed. She knew she needed help. Her employer offered therapy through an online service. Sharice was able to see a therapist on her schedule and be matched quickly. Therapy has helped her manage stress and new ways to cope with her anxiety.

I always thought therapy was too expensive and the wait for an appointment was too long. I’m so glad I was able to connect with a therapist quickly. I’m more centered and prepared for life’s challenges.

- Sharice

Work Solutions

On-the-job benefits can keep employees engaged and motivated. By offering workplace benefits, employers have the opportunity to feel connected and rejuvenated.

- Professional Development

- Cellphone Plan

- Remote Work Credit

- Food Delivery Credits

- Manicures/Massage

- Bring Your Dog to Work

- Nap Pods

- Snack Bar

- New Hire Welcome Package

- Sign-On Bonus

- Home Office Improvement Incentives for Remote Workers

- Casual Dress Codes

- Flexible Work Schedules

- Performance Bonus

- Stock Options

- Leadership Coaching

- Paid Time-off

When Theresa's youngest child wouldn't sleep through the night, she was left exhausted and frustrated. At work, her job created space for nap pods. They weren't the high-tech Google nap pods but a private space with a recliner and couch. Theresa was able to take a short nap while on the clock. After rest, she felt more motivated to finish her work day.

Our nap pods allowed me to get the rest I needed so I could stay motivated on the clock. Sometimes, it’s important to take a step back.

- Theresa

Joe just started a new job that allows him to work from home. His new employer has a home office improvement incentive that allowed him to set up a comfortable space inside his house.

I finally have my dream workspace. I feel comfortable and more productive.

- Joe

Life Solutions

Life happens. Help employees manage their home life with life solution-based benefits.

- Back-Up Daycare Credit

- Tutoring Discounts

- Corporate Discounts

- Unlimited Vacation

- Tuition Reimbursement

- Debt Repayment

- Doggy Daycare

- Pet Savings

- Prepaid Legal Service

- Identity Theft Protection

- Financial Counseling + Financial Planning Resources

- Event and Concert Tickets

- Life Insurance

- Short-term Disability

- Long-term Disability

Emily was the first person in her family to go to college. But during her second year, she had to leave to get a full-time job. With her company's tuition reimbursement program, she could return to school part-time to complete her business degree.

I never thought I would be able to afford to go back to college. My job helped me realize my dream and my family is so proud of me.

- Emily

Throughout most of Amelia’s career, she only had a couple weeks of vacation. It was usually used for family obligations and short travel. When her company switched to unlimited vacation days, Amelia was able to plan her dream vacation overseas.

I never thought I would have enough vacation days to go on a long vacation. I was able to see 4 different countries.

- Amelia

How much do employee benefits cost?

Most employee benefits come at a cost. According to the U.S. Bureau of Labor Statistics, employee benefits are about 30% of total employee compensation costs. It’s important to understand the tax benefits of offering employee benefits. Even some fringe benefits are outlined by the IRS.

How do I calculate the cost of employer-sponsored health benefits for my company?

Offering health benefits to your staff can come with some significant expenses and the dollars can add up quickly. However, to recruit and retain employees, employer-sponsored health benefits may just be the cost of doing business for employers - even if not required to by the ACA (Affordable Care Act).

When calculating the costs of employer-sponsored health benefits, you’ll want to consider several areas of cost. The costs associated with offering employee benefits extend beyond the premium costs. There are costs and work hours associated with setting-up benefits, maintaining, and administering them.

It’s also important to remember that depending on the plan you choose for your employees, those costs may increase year over year. According McKinsey & Company, employers could face health cost increases of 9 to 10% through 2026 because of inflationary pressure passed through from providers. That’s about a 4% increased compared the previous 5 years. The average costs associated with benefits have averaged a 5-7% hike year over year.

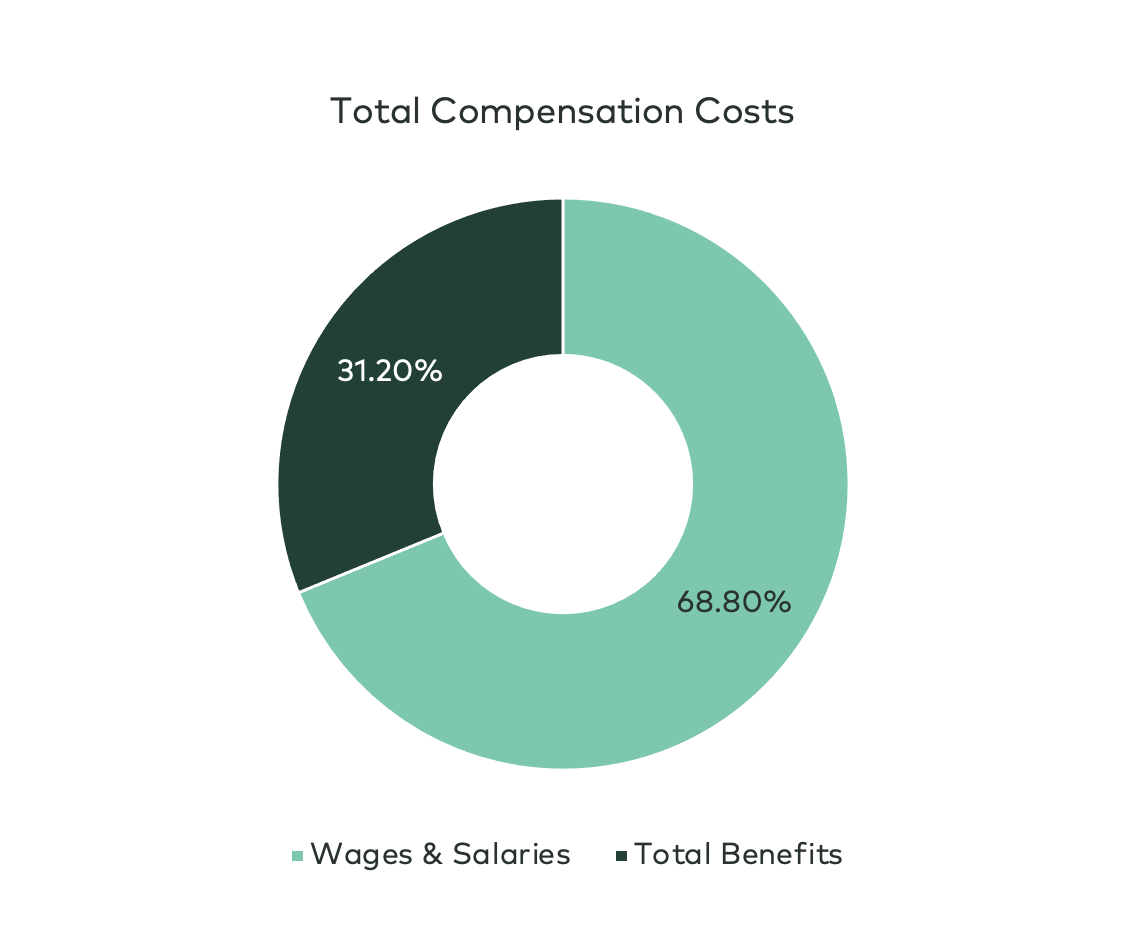

The costs of health benefits will depend on a couple variables: the size of your business and the type of plan you choose and what is covered. Let’s take a look at some data that helps you understand the cost per employee. The U.S. Bureau of Labor Statistics estimates the total employer compensation costs for civilian workers average at $41.86 per hour working in September 2022.

Wages and salaries account for 69% of the hourly wage leaving the remaining 31% at $12.98. It’s important to note that remaining costs include health benefits in addition to other benefits.

However, health insurance is typically the most expensive cost when it comes to benefits. The Kaiser Family Foundation says the average cost of employee health insurance premiums for family coverage was $22,221 and self-only was $7,739 annually in 2021.

How to choose which employee benefits to offer?

With so many benefit options, it’s hard to choose. The best place to start is to align with your company goals. Understand what you what from your company and what type of employer you want to be. The next step would be to understand the needs of your employees. Understanding how to engage your employees is key to driving effective change.

For health benefits, find an HRA administrator that does all the heavy lifting for you, including onboarding employees, reporting, and keeping you compliant. Watch our HRA administration platform demo here!