Small Business Health Insurance Tax Strategy

How can I get a tax deduction for my health insurance?

If you’re a small business owner or sole proprietor, you’ve probably wrestled with how to deduct your health insurance premiums and medical expenses from your taxes. Do you purchase through your business and try to “expense it”? What about a self-employed deduction? And if you have employees—how can I reimburse them without triggering tax consequences?

This guide is designed to help small business owners and sole proprietors discover and implement the most tax-efficient strategy for health insurance and medical expenses.

Small business tax deductions and health insurance

In this guide, we suggest the most tax-efficient strategies for small employers to pursue when purchasing health insurance so that they can maximize their tax deductions. A quick disclaimer—we’re licensed health insurance professionals and small business insurance experts, not tax professionals. Although we share our experience and advice and do our best to cite authoritative sources, you should always seek professional tax advice and not construe anything in this guide as specific tax advice because every situation is different. Ok? Good.

Let’s jump right to it—your best tax strategy will depend on three things:

- Your business entity type

- Whether you work alone or have (or plan to have) W-2 employees

- Whether you’re an owner or an employee

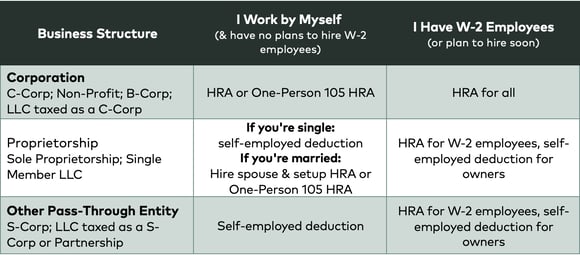

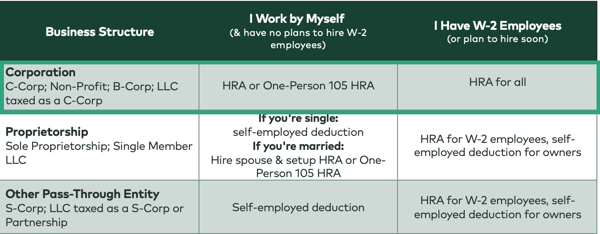

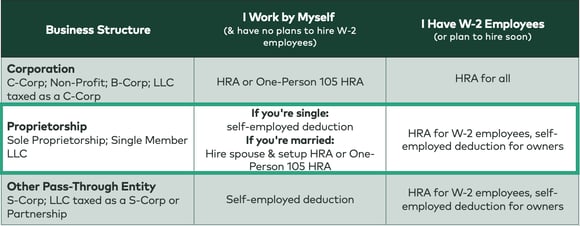

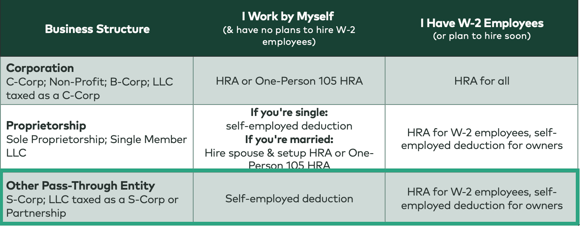

Based on the above, here is a quick table to summarize our recommendations (download a PDF version). The rest of this guide will explain these strategies in more detail. Please be sure to consult with a tax professional before implementing any of these strategies yourself:

Figure 1: Small Business HRA tax strategy overview by business entity type. Download a PDF version of this chart. Not to be used for tax advice. Please consult with a tax professional before implementing any strategy.

This is a bit of a “choose your own adventure” guide, so if you want to skip to the section that applies most directly to you, please feel free to do so. Here’s what we’ll cover:

- Overview of HRAs

- Deep-Dive: One-Person 105 HRAs

- Deep-Dive: Small Business HRAs (QSEHRAs)

- Strategies for a Corporation

- Strategies for a Sole Proprietor

- Strategies for Partnerships & S-Corps

- Next Steps and How to Get Started

Should I reimburse or try to get a group health plan?

What is a Section 105 plan?

A Section 105 plan, often called a 105 HRA, is a health reimbursement arrangement that provides businesses with a tax-advantaged way to reimburse employees for medical expenses. This type of plan is named after Section 105 of the Internal Revenue Code, which establishes the guidelines for employers to make contributions to employee health costs that are tax-deductible to the business and tax-free to the employees.

Under a Section 105 plan, employers can reimburse their staff for qualified health expenses, including co-pays, deductibles, prescriptions, and insurance premiums. These reimbursements are not taxable income for employees, making them a highly sought-after benefit.

Understanding that health insurance can be a business expense is vital for small businesses. Not only is an HRA tax deductible for the business, but it also provides a valuable tool for controlling the cost of health benefits. Small business owners can use a 105 HRA to offer a benefits package that can help attract and retain top talent without the financial burden associated with traditional health insurance plans.

Moreover, Section 105 plans offer flexibility. Employers can design their HRA to fit their company's and employees' specific needs, including setting caps on reimbursements or defining specific categories of expenses that are eligible for reimbursement.

In conclusion, a Section 105 plan is a powerful solution for small businesses looking to manage their health insurance costs effectively. It aligns with the need to make health insurance tax deductible for small business owners, functioning as a strategic business expense that serves the dual purpose of financial management and employee satisfaction.

Benefits of Section 105 Plans

Section 105 plans, also known as Health Reimbursement Arrangements (HRAs), offer several benefits that make them an appealing choice for small business owners. These plans provide financial perks and allow for adaptable health benefit solutions tailored to the business and its employees.

Budget Friendly

One of the most significant advantages of Section 105 plans is their budget-friendly nature. Employers can set fixed allowances for their employees' healthcare costs, which can help stabilize and predict the company's healthcare budget. With this structure, small businesses can provide meaningful benefits to their employees without the unpredictability of rising insurance premiums, making HRAs a financially sustainable option.

Tax Advantages

Section 105 plans come with notable tax benefits. Contributions made by employers are tax-deductible, and reimbursements received by employees are excluded from their gross income, hence not subject to federal income tax. This aspect of HRAs can lead to considerable tax savings for both parties, reinforcing that health insurance is tax deductible for small businesses and that the HRA can serve as a valuable business expense.

Flexibility

Flexibility is a cornerstone of Section 105 plans. Employers can tailor their HRA to match the specific needs of their workforce, deciding on the types of medical expenses that can be reimbursed and setting limits that align with their budgetary constraints. This flexibility also extends to employees who can choose how to spend their healthcare dollars, making HRAs a customizable benefit that can adapt to the diverse needs of a dynamic workforce.

By implementing a Section 105 plan, small businesses can offer a competitive benefits package that is financially and operationally advantageous. This will enhance their ability to attract and retain the best talent while managing costs effectively.

Types of Section 105 Plans

Section 105 of the Internal Revenue Code authorizes several types of plans that allow employers to reimburse employees for medical expenses on a tax-advantaged basis. Each type caters to different business needs and sizes, offering a range of flexibility and control.

HRAs (Health Reimbursement Arrangements)

HRAs are employer-funded health benefit plans that reimburse employees for incurred medical expenses, including individual health insurance premiums. They are highly adaptable, allowing employers to set reimbursement limits and define eligible expenses. HRAs are particularly beneficial for small businesses due to their cost control and tax advantages, making them a popular choice under Section 105 plans.

MERPs (Medical Expense Reimbursement Plans)

Like HRAs, MERPs allow employers to reimburse employees for out-of-pocket medical costs. The primary distinction is that MERPs can be designed to complement existing group health plans by covering expenses not paid by insurance, such as deductibles and co-insurance. This makes them a valuable addition to an employer's health benefits portfolio, enhancing the overall comprehensiveness of healthcare coverage provided to employees.

FSAs (Flexible Spending Accounts)

FSAs are a type of Section 105 plan that allows employees to contribute pre-tax dollars to an account for medical expenses. Employers may also contribute to FSAs, but unlike HRAs and MERPs, FSAs are typically funded through employee salary reductions. FSAs offer the benefit of reducing an employee's taxable income. Still, they often come with the "use it or lose it" rule, meaning employees must use the funds within the plan year or risk forfeiting the remaining balance.

Each of these Section 105 plans offers unique benefits and can be leveraged depending on the specific needs and goals of the small business. Whether it's the comprehensive coverage of an HRA, the supplemental nature of a MERP, or the employee-funded convenience of an FSA, Section 105 plans are versatile tools in structuring effective health benefits.

Section 105 HRAs vs Group Health Plans

We have many clients who initially contacted us asking how they can get a group health plan for their family or a 5-person small business. It used to be that binding a few folks together to “get on the group plan” was the only way to purchase insurance.

Small Business Health Insurance Tax Strategy

How can I get a tax deduction for my health insurance?

If you’re a small business owner or sole proprietor, you’ve probably wrestled with how to deduct your health insurance premiums and medical expenses from your taxes. Do you purchase through your business and try to “expense it”? What about a self-employed deduction? And if you have employees—how can I reimburse them without triggering tax consequences?

This guide is designed to help small business owners and sole proprietors discover and implement the most tax-efficient strategy for health insurance and medical expenses.

Small business tax deductions and health insurance

In this guide, we suggest the most tax-efficient strategies for small employers to pursue when purchasing health insurance so that they can maximize their tax deductions. A quick disclaimer—we’re licensed health insurance professionals and small business insurance experts, not tax professionals. Although we share our experience and advice and do our best to cite authoritative sources, you should always seek professional tax advice and not construe anything in this guide as specific tax advice because every situation is different. Ok? Good.

Let’s jump right to it—your best tax strategy will depend on three things:

- Your business entity type

- Whether you work alone or have (or plan to have) W-2 employees

- Whether you’re an owner or an employee

Based on the above, here is a quick table to summarize our recommendations (download a PDF version). The rest of this guide will explain these strategies in more detail. Please be sure to consult with a tax professional before implementing any of these strategies yourself:

Figure 1: Small Business HRA tax strategy overview by business entity type. Download a PDF version of this chart. Not to be used for tax advice. Please consult with a tax professional before implementing any strategy.

This is a bit of a “choose your own adventure” guide, so if you want to skip to the section that applies most directly to you, please feel free to do so. Here’s what we’ll cover:

- Overview of HRAs

- Deep-Dive: One-Person 105 HRAs

- Deep-Dive: Small Business HRAs (QSEHRAs)

- Strategies for a Corporation

- Strategies for a Sole Proprietor

- Strategies for Partnerships & S-Corps

- Next Steps and How to Get Started

Should I reimburse or try to get a group health plan?

Section 105 HRAs vs Group Health Plans

We have many clients who initially contacted us asking how they can get a group health plan for their family or a 5-person small business. It used to be that binding a few folks together to “get on the group plan” was the only way to purchase insurance.

Because of its legal footing, we believe QSEHRA effectively replaces previous standalone HRA implementations for small business owners and sole proprietors.

You can keep a One-Person 105 HRA and hire other employees if they fall into a category that can safely be deemed “not eligible” for the HRA in the eyes of the IRS. This includes employees under the age of 25, part-time employees (less than 25 hours a week), seasonal employees (less than 7 months a year), or employees with fewer than 3 years of service. Make sure to talk this through with your accountant and attorney. See IRC Section 105(h)(3); Reg. Section 1.105-11(c)(2)(iii)(C).

If you’re the only employee of your business and you have very high medical expenses, you should consider reforming your business as a C-Corp. Yes, you’ll be subject to double-taxation, but all your medical costs can become business expenses, greatly reducing your tax liability. Make sure to talk to your accountant!

Setting up and managing a QSEHRA does not have to cost a lot or add complication to your business. Check out our QSEHRA Administration service. Our fees are nominal compared to your potential tax savings.

What’s the best health insurance if I’m a corporation?

Corporations are the easiest entity type to handle when it comes to health insurance because owners can also be employees. If you’re just getting started, there are obviously other implications with corporations you should talk to your accountant or attorney about.

Health insurance for corporations

Corporations for this discussion include C-Corps, B-Corps, Non-Profits, and LLCs taxed as C-Corps—anything where the entity is separate from ownership. As a corporation, you should be able to get all your insurance premiums and medical expenses counted as a business expense (Schedule C).

Here’s how we suggest Corporations approach health insurance (please consult your tax professional):

Figure 2: Suggested tax strategies for Corporations to maximize healthcare deductions. Download a PDF version of this chart. Not to be used as tax advice. Please consult with your licensed tax professional before implementing any strategy.

Your best strategy will hinge on whether you are the only employee and have no plans to hire in the future or if you have (or plan to soon hire new) W-2 employees. If you are the only employee of the corporation, you can choose between a One-Person 105 HRA or a QSEHRA. We’d recommend:

- If the QSEHRA’s reimbursement limits are enough for you, we recommend going with QSEHRA because it’s much cleaner regulatory-wise (see our HRA Overview section above) and you’re less likely to run into any reporting hurdles.

- If you have high insurance or medical expenses, then you need to go the One-Person 105 HRA route. This is because there are no statutory limits to how much you can expense through your business.

Depending on which strategy makes the most sense for you, please see our Next Steps section below and we can point you towards some resources to get started.

What’s the best health insurance if I’m a sole proprietor?

Health insurance for sole proprietors

Sole Proprietorships are awesome because, well, you’re doing your own thing! It can get a little tricky though because there’s no separation between you and your business in the eyes of the IRS (i.e., you’re a “pass-through entity” or “disregard entity”) and owners are generally not considered to be employees even if you’re working for your company full-time. This includes Sole Proprietorships and Single-Member LLCs that did not elect corporate taxation.

Here’s what we suggest for Sole Proprietors (please consult with your tax professional):

Figure 3: Suggested tax strategies for Sole Proprietors to maximize healthcare deductions. Download a PDF version of this chart. Not to be used as tax advice. Please consult with your licensed tax professional before implementing any strategy.

The best strategy for you depends on whether you have W-2 employees and your marital status (bet you didn’t expect that—we’ll explain). If you’re single and work by yourself, or if you have W-2 employees or plan to hire soon, your best course of action is going to be to take the self-employed deduction for yourself and set up a QSEHRA for your W-2 employees. That will get all your employees’ expenses into the business expense category. Unfortunately, you can’t get your personal insurance and medical expenses categorized that way, but we can still save some tax money by getting all your self-employed deductions. Skip to our Next Steps section to see how.

If you are a sole proprietor and work for yourself and have no plans to hire, and you are married, then we can explore a few more options. Recall from our HRA Overview section that HRAs only work for employees. Although as a proprietor you generally are not eligible for an HRA because you’re not an employee, your spouse can be an employee and eligible for an HRA and health plan that covers you.

Here’s the strategy if you’re a sole proprietor with no employees and you’re married:

- Hire your spouse as a W-2 employee:

- Your spouse’s salary can just be the amount you want to reimburse through the HRA, but it must be a fair wage for what they are doing (i.e., you can’t reimburse $100k through an HRA if your spouse is not actually doing that much work)

- It’s a good idea to have an employment contract and timesheet for record-keeping purposes

- Make your spouse the primary member on your family health plan

- Cover yourself as a dependent on your spouse’s health plan

- Set up a One-Person 105 HRA or QSEHRA for your spouse:

- Choose QSEHRA if you have health expenses that are less than the QSEHRA reimbursement limit ($10,250 as of 2018) or have other employees that are excludable under the QSEHRA regulations so that your spouse is the only eligible employee for the QSEHRA (see the Reimbursement Rules section of our QSEHRA Guide)

- Choose the One-Person 105 option if you have significant medical expenses or have other employees that are only excludable under the One-Person 105 rules (see Pro-Tip in the One-Person 105 HRA section above); the One-Person 105 HRA meets the HRA discrimination requirements because your spouse is the only eligible employee

- Save all your medical bills and records and have your company reimburse the bills each month from a separate account

This strategy only works if you don’t hire any other W-2 employees that would be eligible for either the QSEHRA or One-Person 105 HRA (make sure to look at those rules closely) and assumes that you and your spouse don’t own any other businesses that have employees (common ownership rules would likely apply and the plan would fail to meet Section 105 requirements). You’ll need to keep good records, too. This sounds like a loop-hole and it is, but it’s held up in tax court. The main case was Shellito v. Commissioner. If the above applies, see the Next Steps section for how to get started!

We’ve heard of anchor-spouses for immigration purposes, but we don’t recommend anchor-spouses solely for health insurance tax strategies. Make sure you love them first :)

What’s the best health insurance if I’m a Partnership or S-Corporation?

Health insurance and partnerships, s-corps

If you’re not a corporation and you’re not a proprietor, you fall into this last category we collectively refer to as “Other Pass-Through Entities.” Like proprietors, these are entities where income from your business “passes through” and is reported on your personal tax form. Most of the time, you’re not able to classify yourself as an employee (even if you work for your business full-time) and instead are classified as an owner and required to pay self-employment taxes (talk to your accountant). These entities are typically S-Corps, Partnerships, and LLCs taxed as S-Corps or Partnerships. Note, when we talk about owners of S-Corps, we’re talking about owners with greater than 2% ownership.

Here’s how we suggest Partnerships, S-Corps, and LLCs taxed as such approach health insurance (please consult with your tax professional):

For Partnerships and S-Corps, there’s not a legal way (that we’re aware of) for owners to get their personal insurance and medical expenses counted as a business expense. If you read the Sole Proprietors Strategy section, you might ask, “wait, why can’t I hire my spouse and do what proprietors can do with the One-Person 105 HRA thing?” The problem for S-Corps are that spouses are attributed ownership of the S-Corp. The problem with Partnerships are that there’s more than one person (hence “partnership”) and the One-Person 105 HRA rules fall apart.

If you are a partner in a partnership, your spouse can be hired as a W-2 employee (assuming he or she has no ownership stake in the partnership), and then you can set up the QSEHRA for your spouse and any other W-2 employees.

A good rule-of-thumb when thinking about whether something is deductible as a medical expense is to ask if something is medically necessary or just recommended? Doctor visits and prescriptions are typically necessary and therefore deductible while cosmetic surgery is usually not.