There is new law that can help startups dramatically simplify and reduce costs when offering health benefits to their employees. It's called the 21st Century Cures Act and it created a new tool for employee insurance for small business called QSEHRA. It was backed by Republicans, signed by Obama, and is likely to be a major feature of any Republican plan to replace Obamacare. And no one is talking about it!

It enables a new benefits strategy called "defined contribution," which allows startup owners to offer better benefits for less money and less hassle. Here's how it works and what you need to know.

Health Insurance for Startups

Better benefits for less money? Did I read that right?

With the new law, Congress created a special kind of HRA for small businesses and startups called a QSEHRA (Qualified Small Employer Health Reimbursement Arrangement). The new QSEHRA allows small businesses under 50 employees to reimburse employees tax-free for individual health insurance and medical expenses.

This is a big deal because startups can now get the same favorable tax treatment using a defined contribution strategy but with a lot less hassle than if they tried to purchase a traditional one-size-fits-all small group plan.

What does defined contribution mean?

Defined contribution means you the business owner set an amount each month that you'll reimburse your employees for their own individual policies. Many startups have been doing this, but in the past you'd end up having to pay expensive payroll taxes and your employees would have to pay income taxes. With the new QSEHRA, you can put everything under a tax-free umbrella and dramatically simplify benefits for your company.

→ Read this startup's QSEHRA review for more info about their experience with Take Command!

What's the difference between "defined contribution" and a traditional small group plan?

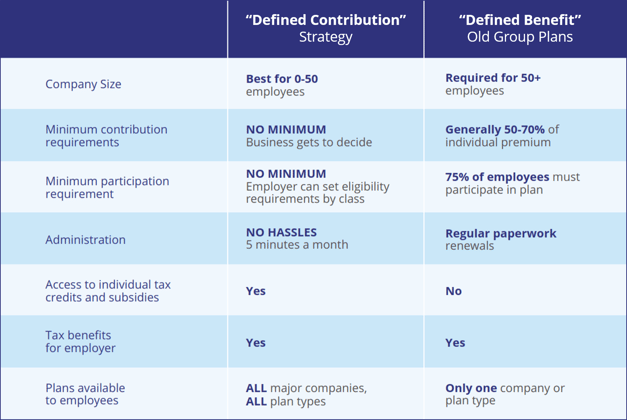

Small group plans are known as "defined benefit" plans because you the owner define how much of a benefit you want to provide (usually in a percentage). This was the old way of doing business but could cause major headaches for startups and small businesses. Defined benefit has become too expensive, inflexible, and unforgiving for startups. However, it used to be worth putting up with because of the favorable tax-status. However, with the new QSEHRA legislation, group plans have lost their major advantage. Here's a handy comparison chart so you can see the differences in the two strategies:

Example: Why "Defined Contribution" works better for startups

With a traditional small group plan, a company chooses a percentage of benefits to cover, i.e., 75%. If a plan cost $1,000, the company pays $750 and the employee pays $250. But what happens if the price goes up? Or employees choose a more expensive plan? The bulk of these rising costs falls on the shoulders of the employer, a burden that is really tough on small businesses whose budgets can be thrown off by unpredictable healthcare costs. In addition, you're locking your employees into a one-size-fits-all plan, with no opportunity for optimization. What if one person's doctor isn't in the network you chose?

Oh, and what happens if you're a small company and someone leaves or opts-out of the plan? Now you're in danger of losing coverage because your participation rate has fallen too low!

With defined contribution, you're taking the burden of choice, administration, and optimization off your plate. You set an amount you want to contribute, and then your employees can shop to find a plan that fits their needs best. Your dollars get optimized as employees select plans that have their doctors, cover their prescriptions, and meet their specific needs without having to overpay. Typically employers can contribute less than they would have with a small group plan and employees can get more. This is a win win!

Take advantage of this new law now!

Does all of this sound complicated? Expensive? Here's some good news. It's a scalable, affordable approach to health insurance for startups. With the right QSEHRA administrator, set up is easy and running it is hands-off.

Hungry for more? Check out the overview chapter in our handy new QSEHRA Guide!

This post was originally written in 2017 and has been updated in 2023 for all of the exciting changes in the HRA world.